Burden of Housing Debt

Here Come the HELOCs: Mortgages, the Burden of Housing Debt, Serious Delinquencies, and Foreclosures in Q3 2024

HELOC balances surged, mortgages not so much, and incomes grew a lot faster than housing debt.by Wolf Richter

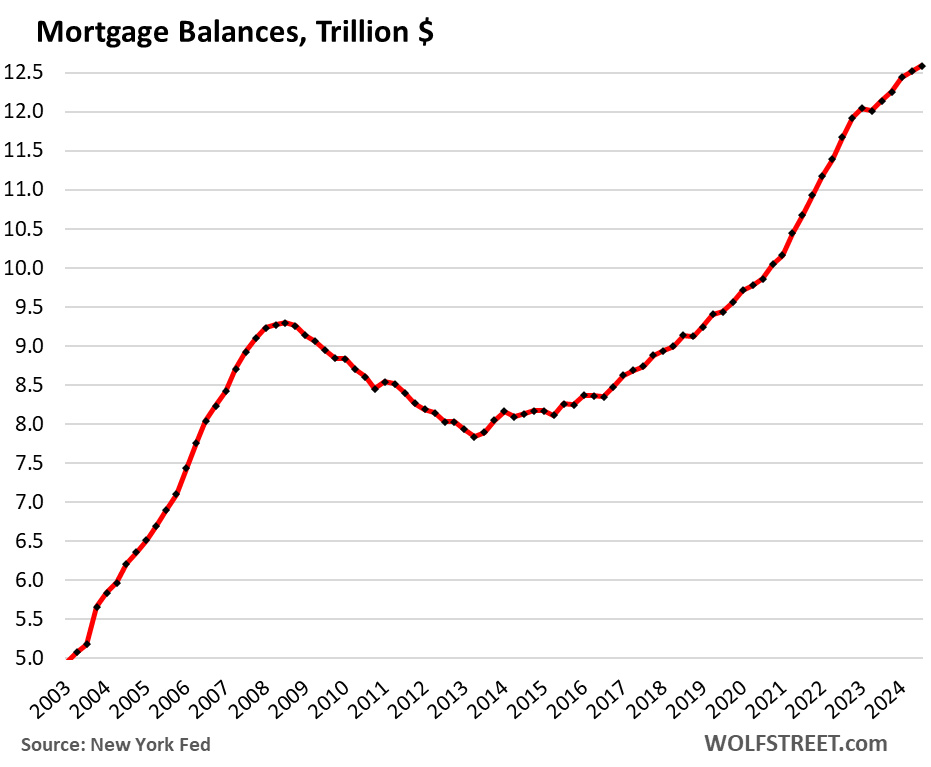

Mortgage balances rose by just $71 billion, or by 0.57% in Q3 from Q2, the smallest percentage increase since the dip in Q2 2023, and the second smallest since 2018, to $12.6 trillion, as demand for existing homes in Q3 plunged to the lowest since 1995, while more and more people who could buy are renting, thereby profiting from an arbitrage between two similar products with very different prices.

Year-over-year, mortgage balances rose 3.8%, according to the Household Debt and Credit Report from the New York Fed, based on Equifax credit reports. The increases over the years were driven by higher prices and thereby larger amounts financed, and peaked at 10% year-over-year during the frenzied Q1 2022 and were above 9% for the rest of 2022. But under the new regime of much higher mortgage rates and too-high prices that have either stalled or are falling, the increases in mortgage balances have slowed dramatically since the end of 2022.

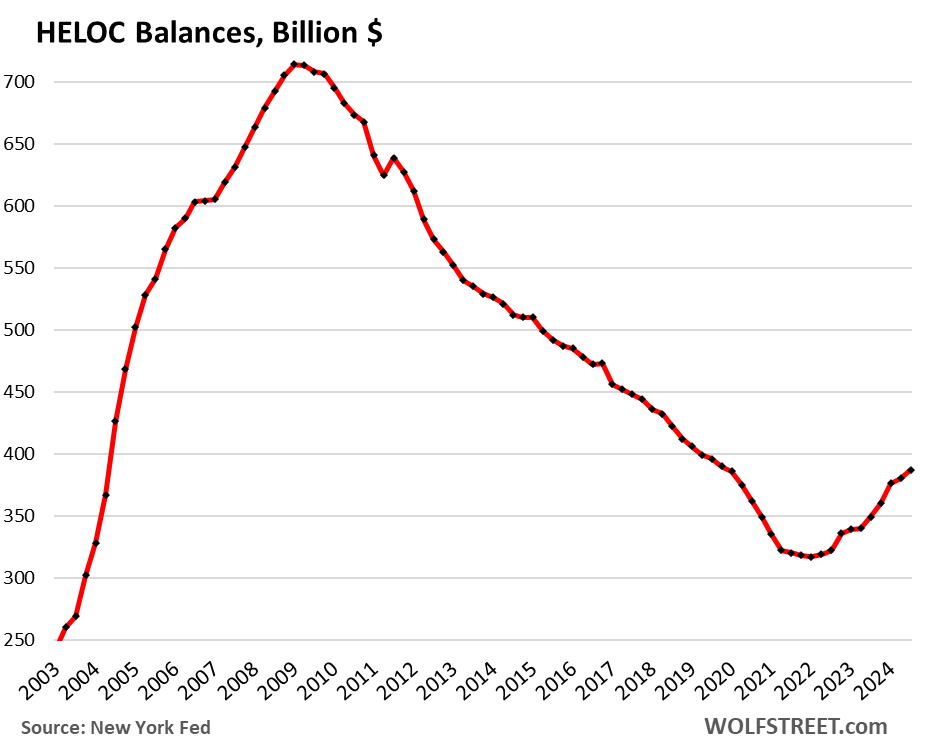

HELOC balances surge.

Balances of Home Equity Lines of Credit jumped by 1.8% in Q3 from Q2, and by 11.9% year-over-year, to $387 billion. Since the low point in Q1 2022, HELOC balances have surged by 22%.

Mortgage refinancings have collapsed due to the higher mortgage rates, and it makes financial sense in this regime, especially for smaller cash-out amounts, to get a HELOC instead of refinancing the whole mortgage plus the cash-out at a higher rate than the original mortgage.

Despite the surge, HELOC balances remain historically low after 13 years of incessant declines. Their share of total mortgage balances has now grown to 3.1%, from 2.8% at the low point. But back in 2005 through 2012, HELOCs amounted to 7-8% of mortgage balances.

HELOCs are a credit line, secured by the home, that homeowners can draw on to turn their home equity into useable cash. They come with interest rates that are generally 2 to 4 percentage points higher than purchase mortgage rates at that point in time – they run close to 10% now – but that’s a lot lower than credit card rates. And only the amount drawn against the credit line incurs interest.

Nearly half of all HELOCs recently originated had credit limits between $50,000 and $150,000, according to a separate report from the New York Fed. That’s the sweet spot for HELOCs. About 28% had credit limits below $50,000, and 25% had credit limits of $150,000 to $650,000. Only 1% had credit limits of over $650,000.

The burden of housing debt.

We’ve compared consumer debt levels to income for a good while now to see where this is going in terms of burden, sustainability, and risk, because we’re always worried about our Drunken Sailors, as we have come to call them lovingly and facetiously, because they’re such a crucial part in the economy.

The income measure we use is “disposable income” from the Bureau of Economic Analysis. That’s after-tax wages plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc., essentially the cash that consumers have available to spend, pay debt service, and save.

And for this purpose of determining the housing-debt burden, we look at mortgage debt and HELOC debt together – housing debts.

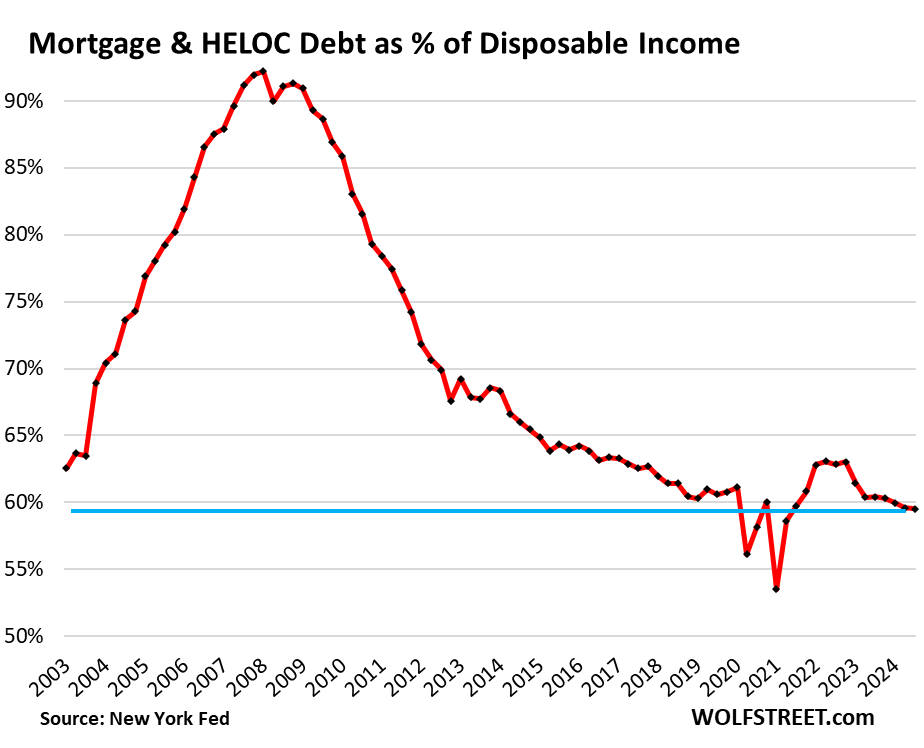

Total mortgage and HELOC debt rose by 0.60% in Q3 from Q2, to 13.0 trillion, and by 3.9% year-over-year.

Quarter-to-quarter, disposable income rose faster (+0.77%) than mortgage and HELOC balances (+0.60%), and so the debt-to-income ratio edged down to 59.5%, the lowest in the data except for the few quarters during the free-money-stimulus era when disposable income was grotesquely inflated.

Year-over-year, disposable income rose 1.6 percentage points faster than housing debt (5.5% vs. 3.9%) and the ratio fell by nearly 1 percentage point.

In the years before and during the housing bust, the housing debt-to-income ratio inflated to scary levels, and when it blew up, it triggered the mortgage crisis that contributed, along with a lot of other leveraged bets, to the near-collapse of the financial system. As consumers dug out of the debris, they deleveraged. And currently their debt burden is relatively low.

On top of the worry list in terms of debts are the federal government and businesses, not consumers.

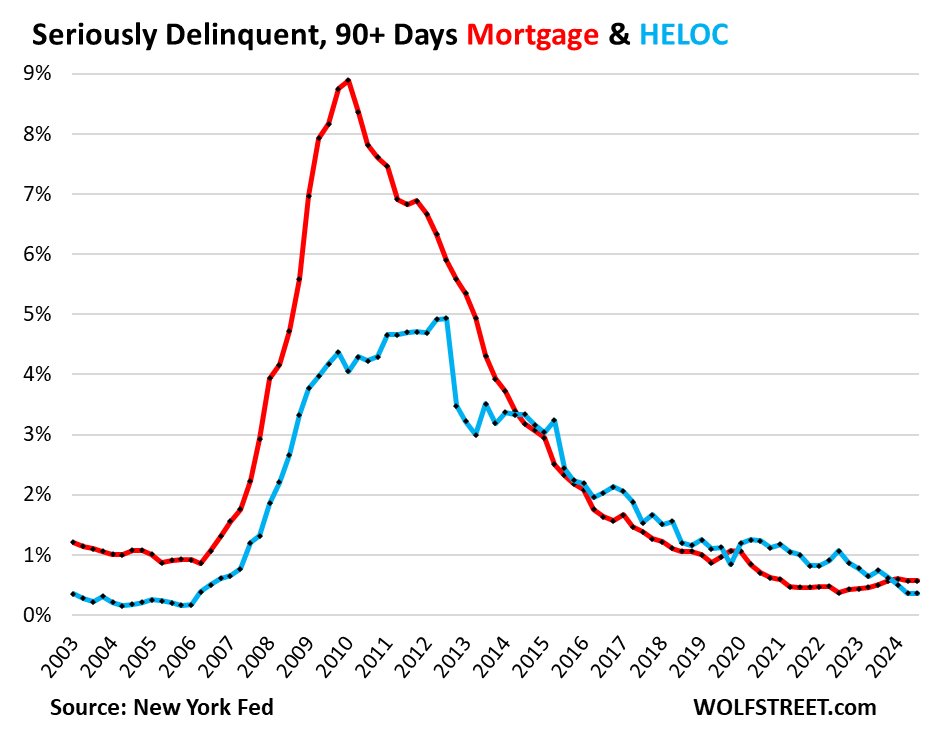

Serious delinquencies remain low.

Mortgage balances that were 90 days or more delinquent remained at 0.57%, well below the range during the Good Times right before the pandemic and before the Financial Crisis, both of around 1% (red line in the chart below).

HELOC balances that were 90 days or more delinquent remained at 0.36%, the lowest since 2006 (blue line).

After the 50% surge in home prices over the past three years, most homeowners, if they get in trouble, can just sell the home, pay off the mortgage and the HELOC, thereby cure the delinquency, and walk away with some cash.

Mortgages don’t get in serious trouble until home prices crater and people lose their jobs at the same time. When that happens, homeowners who can no longer make the mortgage payment cannot sell their homes for enough to pay off the mortgage. That happened during the Housing Bust when home prices plunged, and due to the Great Recession, unemployment spiked to 10%.

Even swooning home prices during a strong labor market don’t trigger a wave of mortgage defaults as homeowners will just quit looking at Zillow every day and continue making their payments.

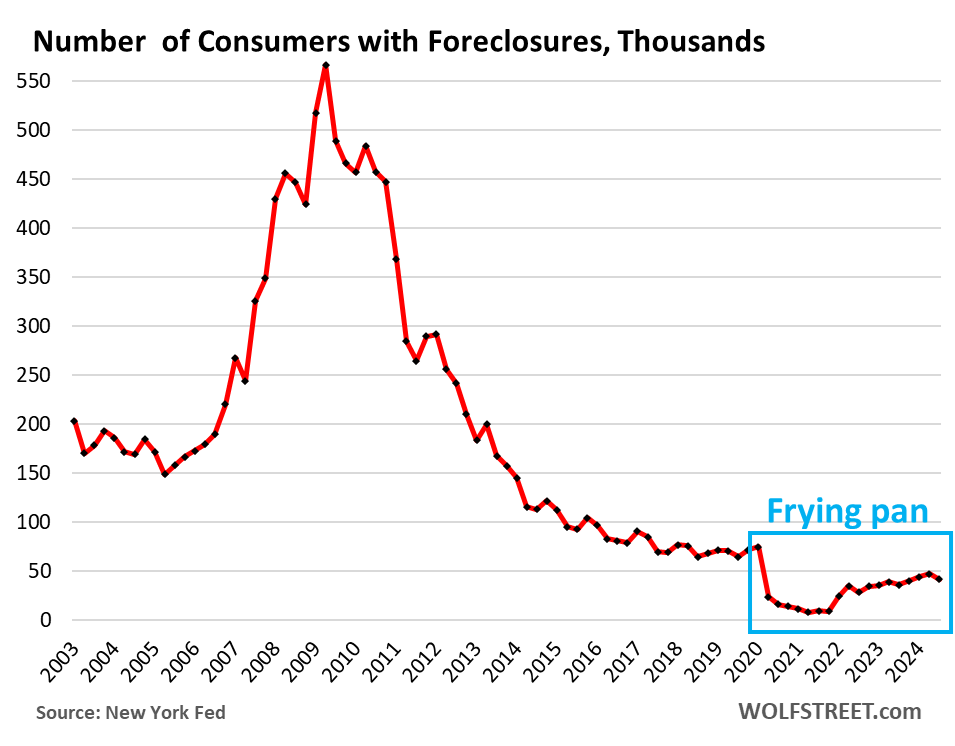

The frying-pan pattern of foreclosures.

The mortgage forbearance programs and foreclosure bans during the pandemic reduced the number of consumers with foreclosures to near zero. They have risen since then but remain well below the prior all-time lows, and in Q3 dipped further, to 41,520 consumers with foreclosures, down from 47,180 in Q2. In the Good Times right before the pandemic (2017-2019), there were between 65,000 to 90,000 consumers with foreclosures.

The post-pandemic frying-pan pattern, as we’ve come to call this phenomenon, has cropped up in other debt-problem data as well:

By Wolf Richter for WOLF STREET.