Unlock your line of credit quote now, featuring guaranteed growth rate!

Reverse Mortgage Line of Credit

In 2023 and now in 2024, the reverse mortgage line of credit continues to be the most popular option for homeowners to access their funds. According to an article by AARP, borrowers recognized this choice about 66% of the time when obtaining a reverse mortgage as being the right choice for them.

The credit line option allows borrowers a great deal of freedom when planning their finances. Homeowners like the fact that they can take as much as they want when the loan originally closes up to the maximum allowed by HUD in the first 12 months and then can take the funds as needed from there.

Borrowers appreciate that while they can take all remaining available funds after 12 months, they are not required to take any funds they don’t want or need. However, since the credit line reverse mortgage is only available at an adjustable rate, many may wonder why this option is even more popular than the fixed rate program.

The answer is flexibility.

Fixed Rate Products Offer Lump Sum Only

The fixed-rate reverse mortgage option has only one way to take your funds, all in a lump sum at the beginning. The fixed-rate does not have a line of credit option; it is a single draw that must be taken in full when the loan closes.

This option is acceptable if you need all the funds at the start, for example, to pay off an existing mortgage or for other purposes. However, if you want to be able to access your funds as you go, the fixed rate option will not work.

The credit line gives the borrowers the option of taking as much money as they wish at initial funding, but then, with the remaining funds, the borrowers can access the funds as they desire. But there are other benefits to the line of credit reverse mortgage as well.

For one, the borrower does not accrue interest on any portion of the funds that are not being used.

Federally Insured LOC = Greater Security

Borrowers who do not need funds immediately do not have to pay interest on the funds if they remain un-borrowed and available to the borrower. The Home Equity Conversion Mortgage (HECM or “Heck-um”) line of credit is the one credit line that can *never be frozen or closed while the borrower still has a remaining balance left on it.

How many people do you know who have had a credit line from their local bank frozen during tough credit times or when home values begin to stabilize or even drop? It may even have happened to you.

The senior HECM borrower with the credit line option has paid their federal mortgage insurance to insure that their line of credit will always be available to them.

(*You must continue maintaining your taxes and insurance and living in your home as your primary residence.)

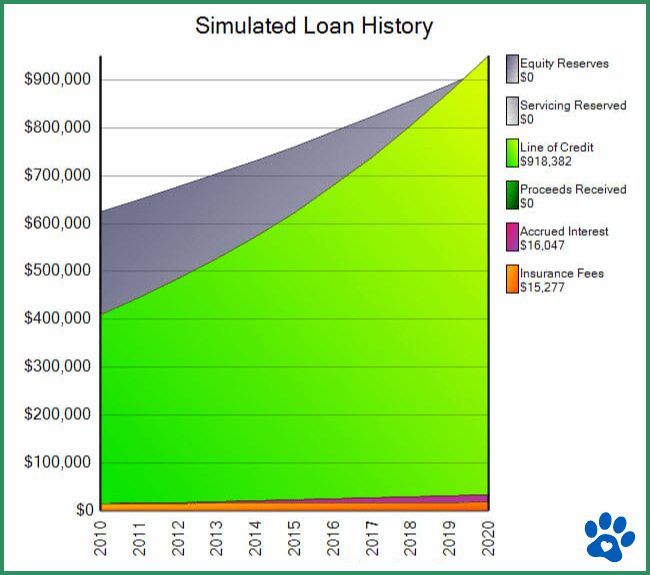

Growth Rate Feature

Another significant feature of the line of credit reverse mortgage is the credit line growth rate.

I have often heard this mischaracterized as interest earned, which it is not. Still, the unused portion of the credit line grows at the same rate at which the loan accrues interest plus the Mortgage Insurance Premium (MIP) renewal.

Growth Rate Example:

In other words, in today’s market, if the fully indexed accrual rate (index + margin) is 4.25%, and the MIP renewal rate that you would add is + .50% = the interest plus the MIP would total 4.75% for the interest and the mortgage insurance combined.

If the Available Loan Amount of your loan is $350,000 after the net Principal Limit and costs have been determined, and you don’t use those funds, then your credit line begins to grow monthly based on the interest rates. Your line of credit would grow by $1,385.41 ($350,000 X .0475 / 12) in the first month alone and would continue to grow at the same rate but would increase as the balance increased.

It would also go down if some or all the funds were used that month, as the unused balance of the funds available determines the growth rate. The following month, you start with a higher loan balance, so the line of credit goes up even higher.

After just five years of this scenario, these borrowers would have available credit of around $450,000 in their credit line, over $550,000 if they were lucky enough to leave it there for 10! And here is a hedge against inflation; as the interest rates rise, the amount the borrowers accrue grows even faster.